IVF cost with insurance: what to ask

IVF cost with insurance can be confusing because “covered” does not always mean “paid for.” That little difference can mess with your whole budget. Your plan may cover testing but not treatment, medication but not embryo freezing, or one cycle with strict rules attached. Before you start making clinic deposits, it helps to compare your benefits against the real treatment costs. My guide to IVF pricing and insurance gives the bigger picture so you can ask better questions and avoid billing surprises.

Insurance can make IVF more affordable. It can also make you feel like you need a law degree and a second cup of coffee just to understand one benefits document.

Let’s make it clearer.

Does insurance cover IVF?

Some insurance plans cover IVF. Many do not. Some cover pieces of fertility care but not the full treatment.

Coverage depends on:

- Your state.

- Your employer.

- Your insurance company.

- Your specific plan.

- Whether the clinic is in network.

- Your diagnosis.

- Prior authorization rules.

- Lifetime fertility benefit limits.

- Medication coverage.

Some states have fertility insurance laws, but the details vary. A state may require certain plans to cover fertility treatment, but that does not mean every person in that state has full IVF coverage. Self-funded employer plans may be exempt from some state mandates.

So if someone says, “My state covers IVF,” take a breath. You still need to check your exact plan.

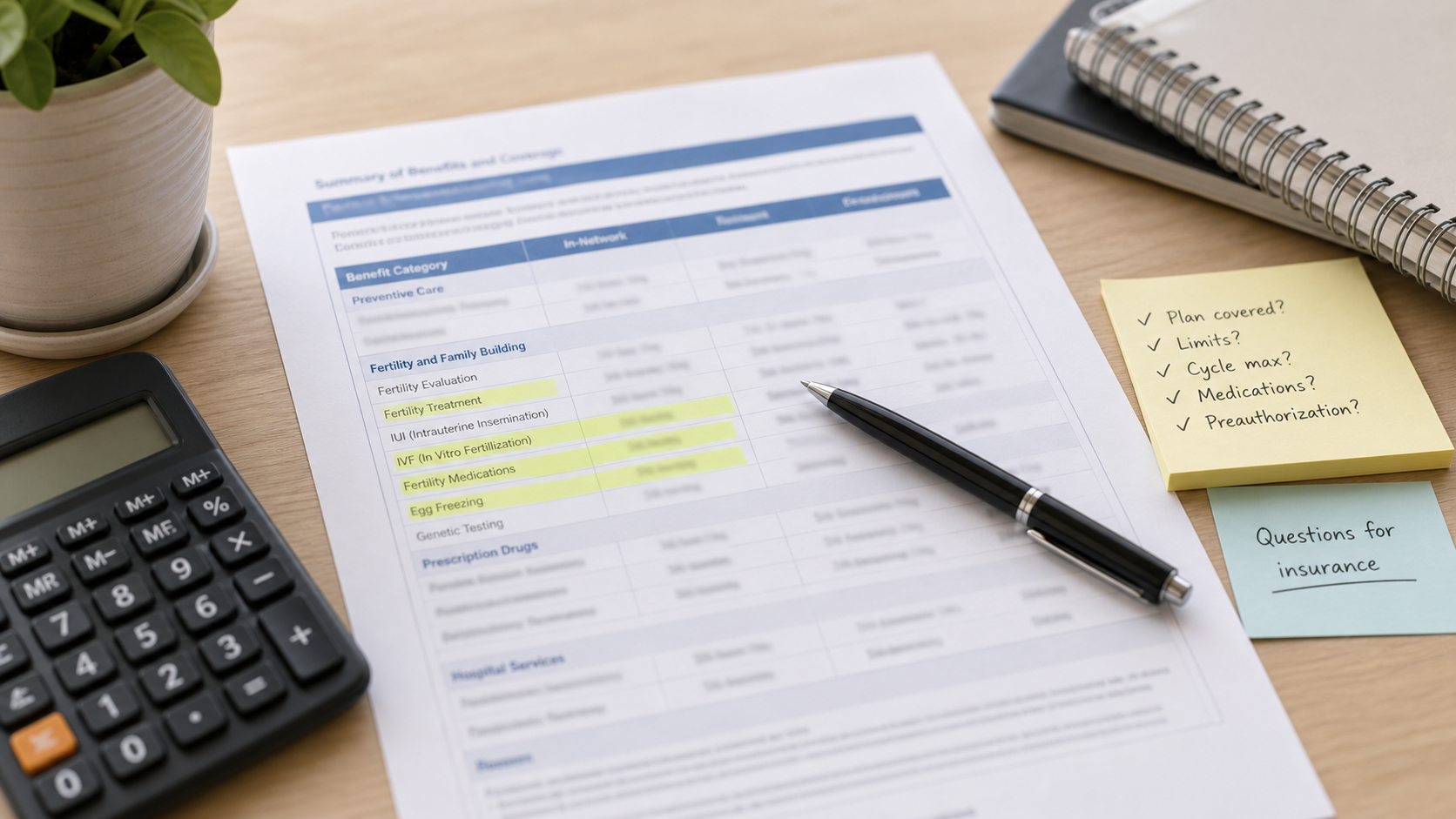

What IVF insurance may cover

Insurance may cover different parts of fertility care.

Possible covered services include:

- Fertility consultation.

- Diagnostic blood work.

- Ultrasounds.

- Semen analysis.

- HSG, a test that checks the uterus and fallopian tubes.

- Saline sonogram, a test that checks the inside of the uterus.

- Monitoring visits.

- Egg retrieval.

- Fertilization.

- Embryo transfer.

- Fertility medications.

- Frozen embryo transfer.

- Pregnancy blood tests.

Some plans cover diagnostic testing only. That means they help figure out why pregnancy is not happening, but they do not pay for IVF treatment.

Some plans cover treatment after you meet certain requirements. Some require a diagnosis of infertility. Some require trying less expensive treatments first, like IUI, which means intrauterine insemination.

Some plans cover IVF but exclude certain add-ons.

This is why you need details. Not vibes. Details.

What may not be covered

Even with IVF coverage, some costs may be excluded.

Common exclusions include:

- Preimplantation genetic testing, often called PGT.

- Embryo freezing.

- Embryo storage.

- Donor eggs.

- Donor sperm.

- Gestational carrier costs.

- Experimental treatments.

- Certain medications.

- Anesthesia.

- Outside lab fees.

- Shipping embryos or genetic samples.

- Fertility preservation without a qualifying diagnosis.

- Extra monitoring outside the clinic.

Insurance can also deny coverage if paperwork is missing or if prior authorization was not done before treatment. That is especially frustrating because the service might have been covered if the approval happened first.

Before you start, ask what is excluded. The “not covered” list is just as important as the covered list.

What “in network” means for IVF

An in-network clinic has a contract with your insurance plan. That usually means negotiated pricing and better coverage.

An out-of-network clinic does not have that contract. You may pay more, or the plan may not cover care there at all.

But fertility billing can get tricky. Your doctor may be in network, but the lab, anesthesia group, genetic testing company, or pharmacy may be separate.

Ask:

- Is the fertility clinic in network?

- Is the doctor in network?

- Is the embryology lab in network?

- Is anesthesia in network?

- Is the genetic testing lab in network?

- Which specialty pharmacy must I use?

- Are outside monitoring clinics covered?

Do not assume one “yes” covers the whole team. IVF involves several moving parts.

Deductibles, copays, and coinsurance

Even if IVF is covered, you may still pay part of the cost.

A deductible is the amount you pay before insurance starts paying for many services. A copay is a set amount you pay for a visit or medication. Coinsurance is a percentage of the cost you pay after the deductible.

For example, if your plan has 20 percent coinsurance, you may owe 20 percent of covered costs after your deductible is met.

That can still be a lot of money when IVF bills are high.

Ask your insurer:

- What is my deductible?

- Has any of it been met this year?

- What is my coinsurance for fertility treatment?

- Are fertility medications under medical benefits or pharmacy benefits?

- What is my out-of-pocket maximum?

- Do fertility costs count toward that maximum?

This is where you may need to be very specific. Insurance representatives may answer differently depending on how the question is worded.

Lifetime fertility benefit limits

Some insurance plans have a lifetime fertility benefit maximum. That means the plan will pay only up to a certain amount for fertility care.

For example, a plan might offer $10,000, $15,000, or $25,000 in lifetime fertility benefits.

That sounds helpful, and it is. But IVF can use that benefit quickly.

Ask:

- Is there a lifetime fertility maximum?

- Is the maximum for medical treatment only?

- Is there a separate medication maximum?

- What has already been used?

- Does monitoring count toward the limit?

- Does genetic testing count toward the limit?

- What happens when the limit is reached?

If medication and treatment pull from the same benefit bucket, you need to know that early. A few high medication bills can eat into the amount available for procedures.

Prior authorization matters

Prior authorization means your insurance company must approve a service before you receive it.

IVF often requires prior authorization. Medications may require it too.

If authorization is missing, insurance may deny the claim even if the treatment would normally be covered.

Ask both the clinic and insurer:

- Is prior authorization required for IVF?

- Is it required for medications?

- Who submits the paperwork?

- How long does approval take?

- What records are needed?

- What happens if treatment starts before approval?

- How will I know approval is complete?

Get confirmation in writing if possible.

I know, paperwork is nobody’s idea of a good time. But prior authorization is one of those boring things that can protect thousands of dollars.

Medication coverage is its own world

Fertility medication may be covered under your pharmacy benefit, medical benefit, or not covered at all.

Your plan may require a specific specialty pharmacy. It may cover some medications but not others. It may require prior authorization for injectable drugs. It may limit quantities.

Ask your insurance company:

- Are IVF medications covered?

- Which medications are covered?

- Which pharmacy must I use?

- Is prior authorization required?

- Are there generic or preferred options?

- Is there a fertility medication maximum?

- Do medication costs count toward my IVF benefit limit?

- What will my copay or coinsurance be?

Then ask your clinic if the prescribed medications match the covered list. If something is not covered, ask whether a medically appropriate alternative exists.

Do not switch medication without your clinic’s approval.

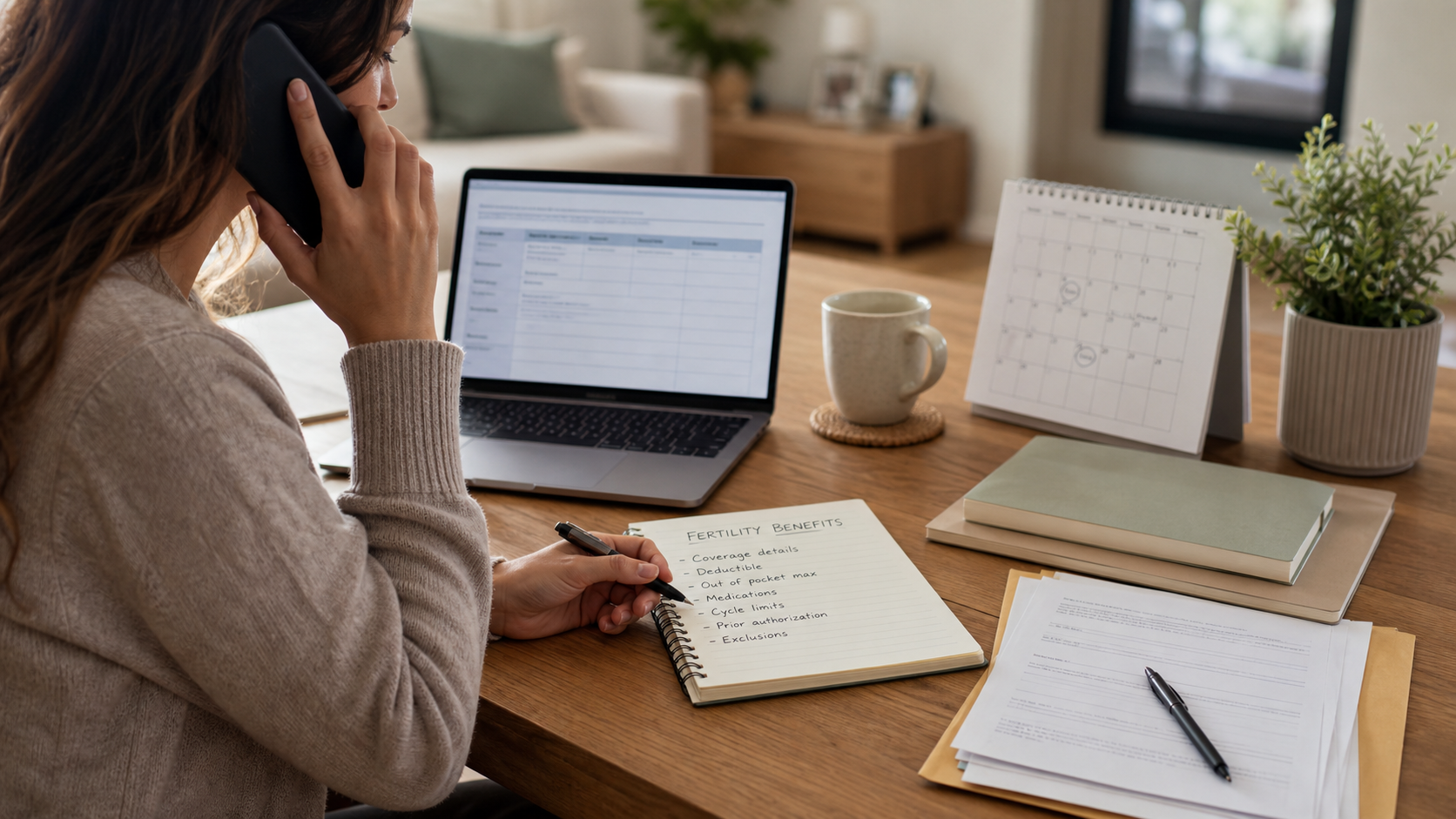

How to talk to your insurance company

When you call insurance, use clear and specific language.

Say you need to verify infertility and IVF benefits. Ask for benefits for both medical treatment and fertility medications.

Have this information ready:

- Your member ID.

- Your plan name.

- Clinic name.

- Doctor name.

- Clinic tax ID or NPI, if available.

- Diagnosis codes, if your clinic provides them.

- Procedure codes, if available.

Ask for a reference number for the call. Write down the date, time, representative’s name, and what they said.

Good questions include:

- Does my plan cover IVF?

- What diagnosis is required?

- Are there age limits?

- Are there cycle limits?

- Are there dollar limits?

- Is IUI required before IVF?

- Is prior authorization required?

- Are medications covered?

- Is genetic testing covered?

- Is embryo freezing covered?

- Is embryo storage covered?

- Which clinics and pharmacies are in network?

If the answer sounds uncertain, call again. I am not saying every insurance call is a little adventure, but okay, sometimes it is.

How the clinic financial team can help

Most fertility clinics have a financial coordinator or billing team. They can help verify benefits, estimate costs, and explain payment timing.

They may know which insurance plans are easier to work with. They may also know common exclusions and authorization rules.

Ask the clinic:

- Can you verify my IVF benefits?

- Can you provide procedure codes?

- Can you give me an itemized estimate?

- What will insurance likely cover?

- What will I owe upfront?

- What happens if insurance denies a claim?

- Do you appeal denied claims?

- Who handles prior authorization?

- What outside companies may bill me?

The clinic’s estimate is not always a guarantee. But it is still useful.

You want both sides: insurance benefit information and clinic billing information.

IVF coverage and state laws

Some states have fertility insurance mandates. These laws may require certain insurance plans to cover fertility diagnosis or treatment.

But the rules vary by state. Some mandates cover IVF. Some do not. Some apply only to certain employers or plan types. Some have age limits, diagnosis requirements, or coverage caps.

Also, employer-sponsored self-funded plans may not have to follow state fertility mandates in the same way fully insured plans do.

That is why state law is only one piece of the puzzle.

If you live in a state with fertility coverage laws, still ask your insurer exactly how the law applies to your plan.

Employer fertility benefits

Some employers offer fertility benefits through companies that specialize in family-building support. These benefits may help with IVF, medication, genetic testing, egg freezing, donor services, adoption, or surrogacy.

Employer benefits may have their own rules.

Ask human resources or your benefits portal:

- Do we have fertility benefits?

- Who manages them?

- What is the lifetime maximum?

- Are medications included?

- Are certain clinics required?

- Is preapproval required?

- Does the benefit cover storage?

- Does it cover genetic testing?

- Does it cover donor services?

- Does unused benefit roll over?

Some people discover benefits they did not know existed. Others discover the benefit is smaller than they thought. Either way, better to know early.

What if insurance denies IVF coverage?

A denial does not always mean the conversation is over.

Ask why the claim or authorization was denied. It may be due to missing records, incorrect codes, lack of prior authorization, plan exclusions, or unmet requirements.

Steps you can take:

- Ask for the denial reason in writing.

- Call the clinic billing team.

- Ask whether an appeal is possible.

- Request corrected codes if there was an error.

- Ask your doctor for a medical necessity letter.

- Check whether employer benefits can help.

- Ask about payment plans or financing if coverage is not available.

Some denials are final because the plan excludes IVF. Others can be appealed.

Stay organized. Keep every letter, bill, reference number, and estimate in one folder.

Questions to ask before starting IVF with insurance

Before treatment begins, ask:

- Is IVF covered under my plan?

- What diagnosis is required?

- Is prior authorization approved?

- What is my deductible?

- What is my coinsurance?

- Is there a lifetime fertility maximum?

- Are medications covered separately?

- Is the clinic in network?

- Is the lab in network?

- Is anesthesia covered?

- Is ICSI covered?

- Is PGT covered?

- Is embryo freezing covered?

- Is storage covered?

- Is frozen embryo transfer covered?

- What will I owe before treatment starts?

- What could be billed later?

If you can get the answers in writing, do it. Future you will be grateful.

Conclusion

IVF cost with insurance depends on your plan, state, employer, clinic, diagnosis, and treatment details. Insurance may cover testing, medication, monitoring, egg retrieval, transfer, or only some pieces. You still need to check deductibles, coinsurance, lifetime limits, prior authorization, network rules, and exclusions like genetic testing or embryo storage.

If your plan does not cover enough, the guide on IVF financing options can help you compare payment plans, loans, grants, and employer benefits. For the full treatment cost breakdown, return to the main IVF cost guide.

Table of contents

- Does insurance cover IVF?

- What IVF insurance may cover

- What may not be covered

- What “in network” means for IVF

- Deductibles, copays, and coinsurance

- Lifetime fertility benefit limits

- Prior authorization matters

- Medication coverage is its own world

- How to talk to your insurance company

- How the clinic financial team can help

- IVF coverage and state laws

- Employer fertility benefits

- What if insurance denies IVF coverage?

- Questions to ask before starting IVF with insurance

- Conclusion